Scaling in Europe: How to Deploy a Compliant Spain Crypto Payment Gateway

⏱️ TL;DR:Spain is becoming a high-growth Web3 hub under MiCA 2.0. As legacy fiat rails fail under high fees and fraud risks, deploying a scalable, compliant European crypto payment gateway is now a core requirement for cross-border growth in the EU market.

Spain & MiCA 2.0: The New Epicenter for Web3 Payments

The era of the "Wild West" in cryptocurrency is officially over, giving way to a new paradigm where digital assets are integrated into the core financial infrastructure. The European Union is leading this charge, solidifying its regulatory perimeter under the Markets in Crypto-Assets (MiCA) 2.0 framework. For forward-thinking operators, this isn't a hurdle—it is a massive pre-regulatory dividend.

At the heart of this European Web3 and digital entertainment expansion is Spain. Compared to other regional markets, Spain’s ecosystem remains notably more crypto-native, particularly across iGaming and prediction communities. This boom is being heavily catalyzed by massive sporting events like the upcoming FIFA World Cup.

To capture this influx of Web3-native liquidity—where high-net-worth "whales" deposit hundreds of thousands in USDC or USDT—merchants desperately need robust operational capabilities, including instant settlement, stablecoin routing, and multi-chain flexibility. This is no longer a user acquisition problem; it is a payment infrastructure scalability problem.

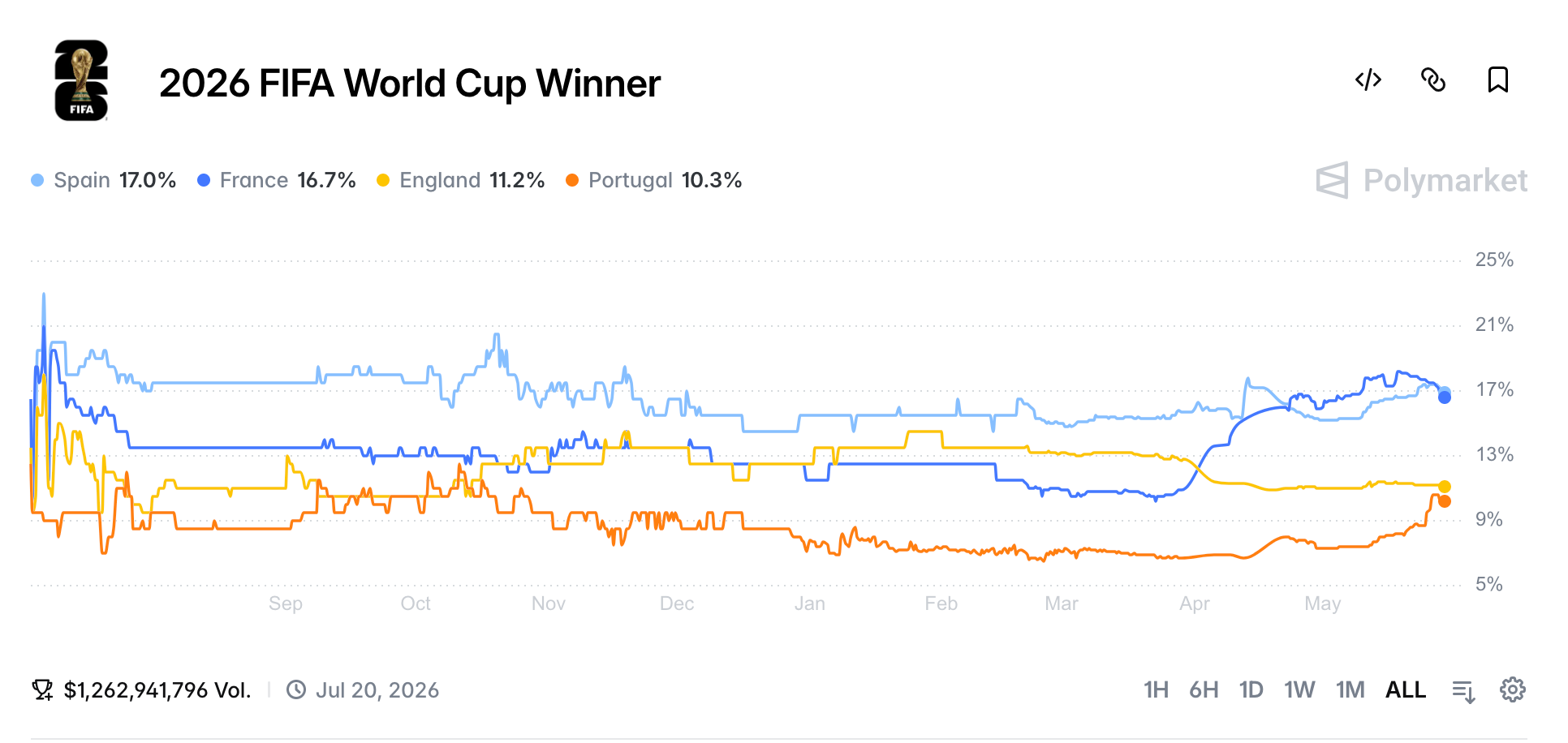

Looking at global prediction markets like Polymarket, Spain currently commands a leading probability of taking the trophy. This sporting dominance translates directly into massive financial volume. To capture this influx of Web3-native liquidity—where high-net-worth "whales" deposit hundreds of thousands in USDC or USDT—merchants desperately need robust operational capabilities, including instant settlement, stablecoin routing, and multi-chain flexibility. This is no longer a user acquisition problem; it is a payment infrastructure scalability problem.

The Hidden Cost of Legacy Payments in the EU

While the traffic surge presents an incredible opportunity, it exposes the fatal flaws of traditional financial routing. Relying exclusively on fiat gateways presents severe friction for cross-border merchants:

The Impact of Cross-Border Fees

When international users attempt to purchase digital goods on a Spain-based platform using traditional credit cards, legacy processors typically enforce:

- Direct transaction fees ranging from 2.9% to 5%.

- Opaque foreign exchange (FX) conversion spreads.

- Rolling reserve requirements that can lock up business cash flow for up to 180 days.

The Chargeback Trap and Friendly Fraud

Beyond basic transaction fees, chargeback disputes—often classified as "friendly fraud"—represent one of the biggest daily headaches for operators. In high-velocity sectors like iGaming and SaaS, a user can deposit via credit card, consume the service, and maliciously file an unauthorized use claim. The merchant loses the initial revenue and gets hit with a $25 to $50 penalty fee.For a platform operating on a standard 10% net profit margin, a single $50 chargeback penalty can easily wipe out the revenue of 10 to 15 legitimate sales. The real cost is not only transaction fees; it is margin erosion at scale.

Why Compliance Is Becoming Core Payment Infrastructure Under MiCA 2.0

As MiCA implementation accelerates across Europe, payment infrastructure is no longer just a technical decision. It is increasingly becoming a strict compliance requirement. For merchants expanding into Spain and broader EU markets, two operational realities are rapidly emerging:

Restricted Access for Non-Compliant Platforms

Historically, some offshore crypto platforms accessed European users through regulatory gray areas such as "reverse solicitation." Under MiCA, these pathways are becoming increasingly limited. Relying on payment providers without recognized EU compliance frameworks may result in growing restrictions when servicing European users.

This shift is already visible across Spain’s digital entertainment sector. In May 2026, Spanish regulators temporarily blocked access to prediction market platforms Polymarket and Kalshi over allegations that the operators lacked the required local compliance safeguards. This signals a broader transition: infrastructure without localized compliance frameworks is becoming increasingly difficult to scale sustainably.

The Expanding Regulatory Scope of Digital Assets

The rapid rise of prediction markets and tokenized digital entertainment has introduced new legal complexity across Europe. While regulators continue debating how certain event-based contracts should be classified, the underlying transfer of crypto-assets increasingly falls within EU-aligned oversight.

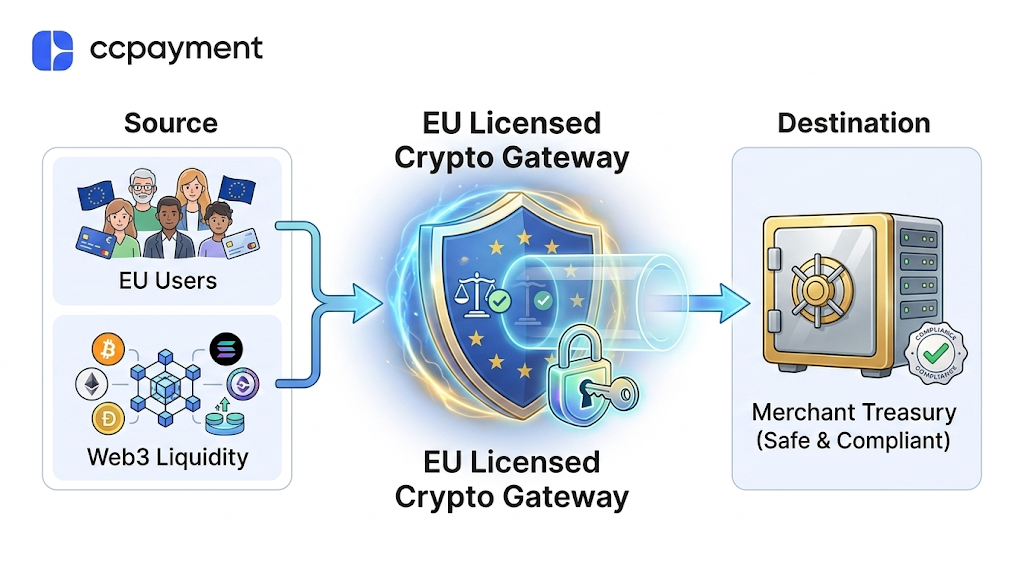

For operators, this creates a simple reality: payment interruptions, frozen settlement flows, or restricted access to EU users can quickly become operational risks. Rather than internally managing evolving AML, KYC, and stablecoin classification requirements, forward-thinking merchants are relying on licensed digital asset infrastructure capable of abstracting this regulatory complexity entirely.

What Merchants Should Look for in an EU Licensed Crypto Gateway

As the MiCA framework standardizes European crypto operations, selecting the right payment infrastructure becomes a critical compliance decision.

When evaluating options, operators generally consider three categories:

| Infrastructure Category | Legacy Fiat Gateways (e.g., Stripe, PayPal) | Local Regional VASPs(e.g., Bit2Me) | Enterprise Web3 Infrastructure(e.g., CCPayment) |

| Processing Costs | High (2.9% - 5% + FX spreads) | Moderate (1.0% - 2.5%) | Optimized (Starting at 0.2%) |

| Chargeback Exposure | Severe (Merchant liability + fees) | None (Immutable) | None (Immutable) |

| Asset Coverage | Fiat only | Limited (Top 20-50 tokens) | Comprehensive (900+ assets) |

| Regulatory Alignment | Traditional Financial Licenses | Regional Registrations | Fully EU-Licensed |

| Settlement Efficiency | Delayed (T+2 to T+5 days) | Moderate (Varies by banks) | Instant (Real-time conversion) |

As the comparison demonstrates, traditional fiat gateways cripple merchants with high fees and systemic fraud risks. Local regional crypto exchanges, while compliant, often lack the technological depth to support a truly global Web3 audience. To navigate the market effectively, merchants typically rely on enterprise infrastructure capable of multi-chain routing and instant stablecoin settlement.

How a MiCA Compliant Payment API Simplifies Stablecoin Settlement

Understanding MiCA compliance is important, but executing it efficiently at the checkout level is what keeps the business running. Integrating a regulated MiCA compliant payment API provides several direct operational advantages:

- Multi-Chain Flexibility: To help users bypass high Ethereum network fees, our payment gateway provides comprehensive support across multiple alternative blockchains, including Polygon, BSC, and Arbitrum. By giving customers the freedom to choose their preferred, low-cost network at checkout, businesses can significantly reduce transaction friction and minimize cart abandonment.

- Unlocking Long-Tail Liquidity: By integrating an API that supports over 900 cryptocurrencies, businesses stop artificially restricting their user base to only Bitcoin or Ethereum whales.

- Automating Treasury Stability: Managing corporate treasury volatility is a primary concern. Modern gateways address this by instantly converting volatile token payments into price-stable assets such as USDC, helping businesses reduce exposure to crypto market volatility.

The accounting team receives more predictable revenue streams, while compliance is assured by the provider's EU licenses.

Preparing for Cross-Border Growth in Europe’s Regulated Crypto Economy

As markets like Spain solidify their position in the European Web3 ecosystem, overseas merchants are evaluating their operational readiness. Relying exclusively on traditional fiat gateways presents significant friction, while fragmented regional providers struggle to deliver necessary multi-chain scalability.To capture this influx of Web3-native liquidity, merchants must integrate compliant stablecoin settlement and global routing within a unified stack.

Secure your European expansion with a robust Spain crypto payment gateway powered by CCPayment’s global ecosystem.

FAQ

Q1: What is a MiCA compliant payment API?

A: A MiCA compliant payment API refers to crypto payment infrastructure designed to align with the European Union’s Markets in Crypto-Assets (MiCA) framework. These APIs typically support compliant stablecoin settlement, AML/KYC workflows, multi-chain payment routing, and EU-aligned operational standards. For SaaS platforms, iGaming operators, and digital merchants, utilizing a MiCA compliant payment API helps simplify cross-border crypto payments while reducing regulatory and operational friction.

Q2: Is crypto payment legal in Spain under MiCA?

A: Yes. Crypto-related business activity is fully legal in Spain under existing EU frameworks. However, as MiCA implementation progresses, businesses are increasingly shifting toward compliant infrastructure providers that possess valid EU licenses to ensure long-term operational stability.

Q3: What exactly is a zero chargeback EU gateway?

A: A zero chargeback EU gateway refers to crypto-native payment infrastructure where transactions are settled on a blockchain. Because blockchain transactions are cryptographically final and immutable, users cannot force a bank reversal. This structurally eliminates the traditional card-based "friendly fraud" that plagues digital merchants.

Q4: Why are European merchants adopting stablecoin settlement instead of fiat?

A: Merchants use stablecoins such as USDC and USDT to reduce cross-border banking delays, bypass opaque FX conversion spreads, and maintain 24/7 treasury flexibility. It offers the stability of fiat with the speed of Web3.

Q5: What does the upcoming MiCA 2.0 framework mean for SaaS and iGaming operators?

A: The evolving MiCA framework is expected to introduce clearer definitions regarding e-money tokens (EMTs) and multi-issuance schemes. For operators, it means the underlying payment APIs they use must be robustly compliant and capable of automatically navigating these complex classifications without disrupting the user checkout experience.

Crypto Adoption for Business 2026

Deep dives into Web3 payments, industry trends, and how to scale your global commerce with zero-code integrations.