How to Accept USDT for Virtual Card Top-Up with CCPayment

⏱️ TL;DR: CCPayment helps virtual card issuers move beyond consumer card rails and build a stablecoin-based top-up layer designed for margin protection, faster reloads, and production-ready integration.

Why Virtual Card Platforms Need a New Funding Layer

Virtual card platforms are not losing ground because demand is weak. They are losing margin because the funding layer was never designed for them. Card fees, chargebacks, and cross-border processing costs were built for consumer retail — not for frequent, small-value reloads where every basis point compounds across volume.

When a platform relies on rails built for consumer card payments, it inherits fixed fees, fraud exposure, and settlement delays that can make small reloads expensive to process. If you are building a cross-border VCC product, you need a payment layer designed for crypto-native top-ups, not another fiat rail wearing a new interface.

This is where accepting USDT for virtual card top-ups can change the economics. USDT can provide a lower-friction funding path for frequent reloads, while the right architecture helps keep the system secure, auditable, and production-ready. In practice, that means permanent deposit addresses, webhook-driven confirmations, stablecoin settlement, and idempotent server-side processing.

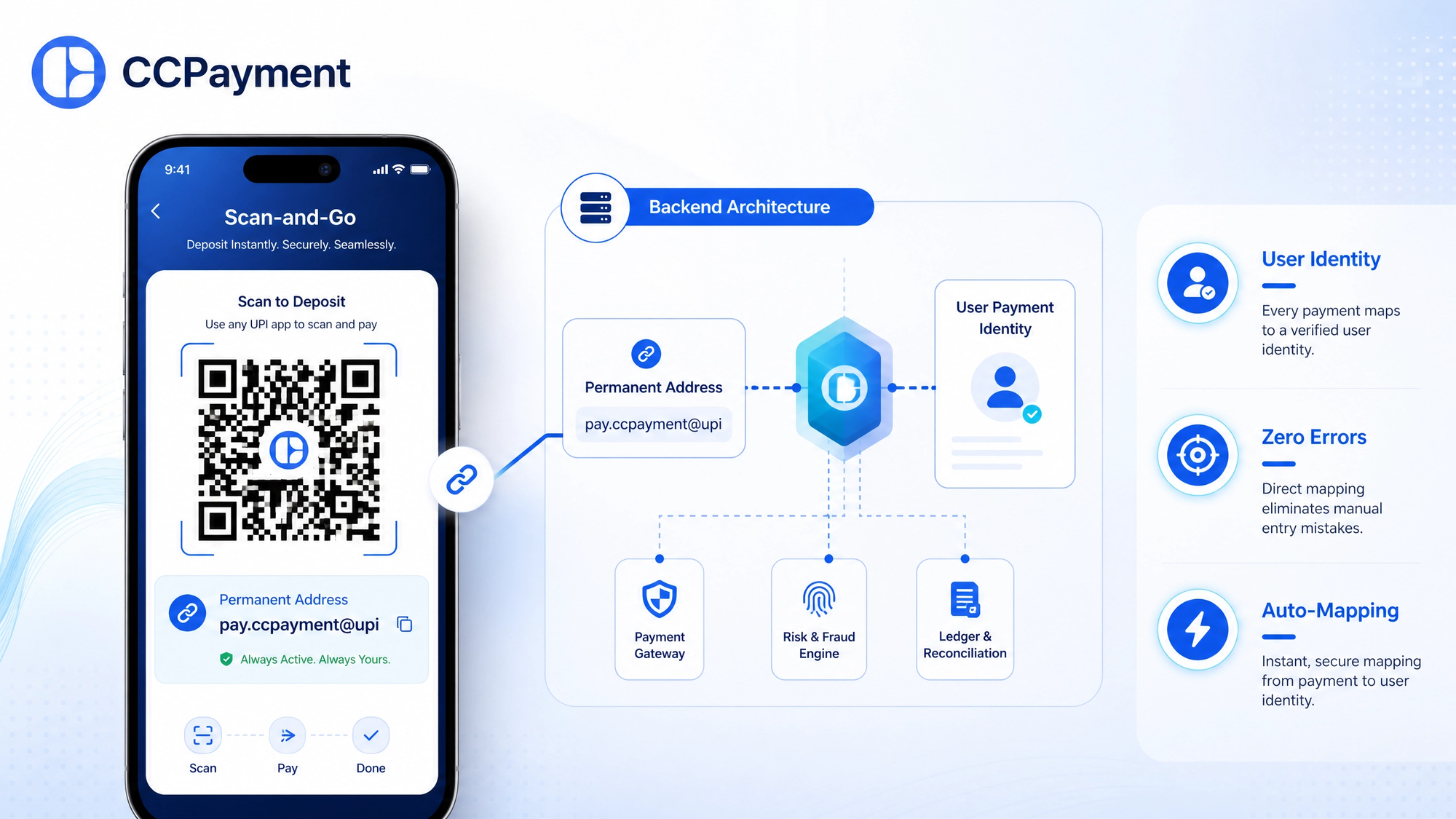

User Journey: From QR Code Scan to Card Swiping

For cardholders, the reload experience can be simple: open the app, scan a QR code or tap a deposit link, send USDT, and see the virtual card balance update quickly. Every extra step—switching addresses, guessing the right network, or waiting for manual review—can reduce completion rates.

To make that flow work at scale, the backend needs to be built around account-centric permanent deposit addresses, not one-time invoice addresses. With CCPayment’s Permanent Address mode, each user gets a deposit address that stays stable over time, plus a memo or tag where the chain requires one.That design helps in three ways:

- The address can become part of the user’s payment identity.

- Repeat top-ups can become easier and less error-prone.

- Your backend can map deposits directly to user accounts without rebuilding the flow every time a customer returns.

On the front end, this translates into a clean scan-and-go experience. The user sees one address, one network choice, and one clear status path. Behind the scenes, your system tracks the account relationship, while CCPayment handles the chain-side monitoring and emits webhook events when a confirmed deposit arrives.

Unified Infrastructure Matters More Than Chain-by-Chain Complexity

If you are designing a stablecoin funding layer, the TRC20 vs ERC20 question will come up — but it should not become an infrastructure decision you rebuild for every chain. Tether's official transparency data shows that USDT is widely circulated across major networks, but those networks behave differently in real usage.

For merchants, the trade-off is usually straightforward:

- USDT ERC20 can offer strong ecosystem familiarity and deep institutional acceptance, but gas fees can become painful for frequent small reloads.

- USDT TRC20 often offers lower fees and faster confirmations, which can make it attractive for the $10–$200 range common in virtual card top-ups.

This is why the "best" network is not a universal answer. It depends on your customer profile, ticket size, and tolerance for confirmation delay. If your audience is mostly reload-heavy and cost-sensitive, TRC20 often becomes the default. If you serve more institutional or DeFi-linked users, ERC20 may still matter. Either way, CCPayment supports both networks under the same integration, so the choice stays a business decision rather than an engineering one.

The bigger point is that you should not need to run separate nodes, chain-specific monitoring services, and fragile queue logic just to support both options. CCPayment’s Unified REST API abstracts that complexity:

- One integration for supported deposit networks.

- One webhook model for deposit status updates.

- One operational layer handling chain confirmation logic and reorg tolerance.

That can reduce engineering overhead and help your team stay focused on the actual product: card funding, balance management, and risk policy.

Compliance & Risk Management: KYT and Webhook Security

Accepting USDT for virtual card top-ups is not only a payment decision. It is also a compliance decision. USDT flows often sit in regulated environments where KYC, regional restrictions, and transaction monitoring matter just as much as UX.

A production-grade VCC platform usually needs at least three layers of control:

- Regional restrictions: based on your licensing footprint and banking partners.

- User-level KYC linkage: so top-up behavior can be tied to verified accounts.

- Blacklist and risk scoring workflows: for suspicious addresses, patterns, or counterparties.

CCPayment supports this model with real-time KYT screening. Incoming deposits can be evaluated through KYT, and risky transactions may be flagged before the merchant credits balance., and risky transactions can be flagged. That means your risk engine can decide whether to approve, delay, or review a top-up before it affects the card balance.

Security is equally important in the webhook layer. One of the most common mistakes is trusting deposit notifications blindly. To reduce the risk of fake deposit webhook attacks, the safer pattern is:

- Use amount-less webhooks to signal that an event occurred.

- Verify the webhook signature server-side with HMAC.

- Call the Get Deposit Record API to fetch the authoritative amount, asset, network, and transaction hash before crediting the user.

This approach adds one extra server-to-server lookup, but it prevents spoofed payloads from creating false balances. For any fintech product, that trade-off is worth it.

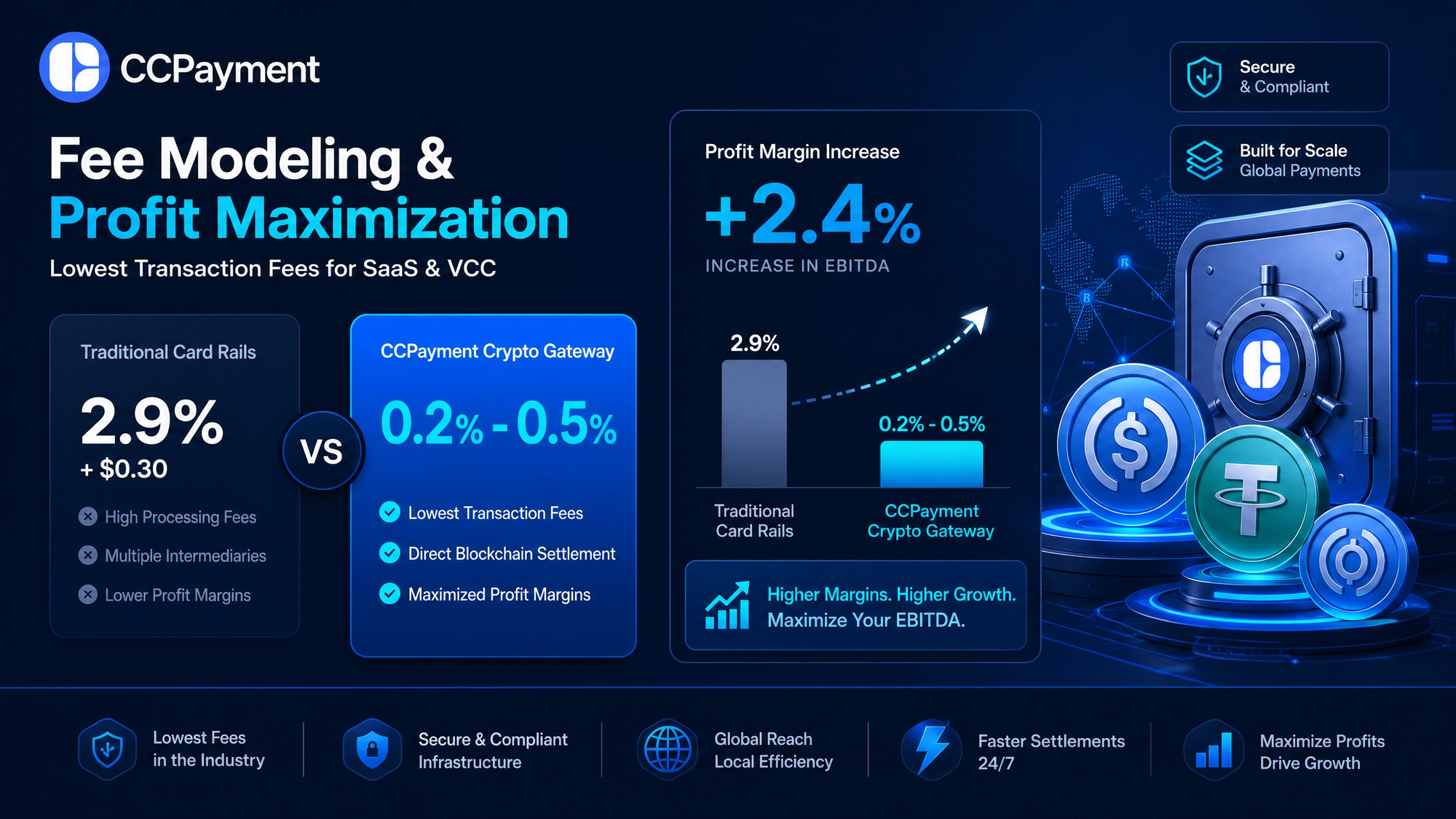

Why Margin Protection Is the Real KPI

The economics of a virtual card platform are not decided at checkout. They are decided at the funding layer. Every point of cost — gateway commission, gas, FX spread, settlement delay — compounds across reload volume before a single card is swiped. Traditional card rails often charge 2.9% + $0.30 or more once you include processing and cross-border overhead. For small reloads, that fixed fee becomes a large percentage of the transaction size. When you add chargebacks, operational review, FX spread, and settlement delays, effective net margin on a reload can narrow significantly.

USDT changes that equation, but only if the rest of the stack is designed correctly. The goal is not just to “accept crypto.” The goal is not just to "accept crypto." The goal is to build a stablecoin funding layer where margin is protected by design — not recovered after the fact through pricing adjustments.

CCPayment’s fee structure is built around that logic:

- 0.2%–0.5% tiered gateway fees on supported flows.

- No extra fixed per-transaction crypto fee like a card processor would impose.

- An Estimate Network Fee API so you can show or absorb gas costs depending on your pricing model.

That gives you flexible cost allocation:

- Merchant-funded gas keeps the user experience simple and conversion-friendly.

- User-funded gas makes the pricing more transparent and can protect margins on lower-value reloads.

If you also convert incoming funds into a preferred stablecoin, your treasury gains another layer of protection. Stablecoin settlement reduces exposure to volatility and lets finance teams keep the reload pipeline aligned with operational cash needs.

Production-Ready Payment Flow for Edge Cases

In production, not every user will pay the exact amount, at the exact time, on the exact network. Edge cases are not exceptions — they are part of the operating model.

That is why you need a plan for underpaid or expired crypto invoices before launch. CCPayment’s Order mode helps here by locking the exchange rate for a defined window and giving you a structured invoice lifecycle.Typical fail-safes include:

- Invoice expiry windows, so old payment links do not stay open forever.

- Manual review queues for edge cases that are economically valid but operationally ambiguous.

Your backend should also be built for webhook retries and duplicate deliveries. The same payment event may arrive more than once, so your system must be idempotent. The standard pattern is simple:

- Treat the on-chain txId (transaction hash) as your idempotency key.

- When you receive a deposit notification, first query your database by txId to check whether that transaction has already been recorded.

- If the txId exists, skip any further business processing or balance updates.

- If the txId does not exist, let your backend decide whether and how to credit the user.

Before going live, you can validate all of this in the CCPayment Testnet Sandbox. It lets your team test deposit address generation, webhook handling, order expiry, and edge-case logic without real funds, KYC bottlenecks, or IP whitelisting constraints.

Why This Architecture Works as Enterprise Infrastructure

A production-grade stablecoin funding layer does more than move money. It protects margin by design, reduces operational overhead through unified infrastructure, and delivers a predictable experience that scales with volume. Permanent deposit addresses lower friction. Webhooks make the system responsive. Stablecoin settlement keeps treasury cleaner. Idempotency protects your ledger.

This combination makes crypto payment infrastructure production-ready for VCC platforms. It's not about replacing one payment rail—it's about building a top-up layer that fits virtual card economics and risk profiles.

For cross-border VCC founders, fintech PMs, and Web3 technical leads, this is the fastest path from architecture to working crypto top-up code. The same unified Web3 infrastructure you build for users can help you build faster and more reliably.

Your virtual card platform already has demand. The remaining gap is a top-up layer that supports your margin model. Give your users a clearer reload experience and your business a payment stack that aligns with your financial targets.

👉 Create Your CCPayment Account and Start with a 0.2% Rate Today

FAQ

Q: Why should a virtual card platform accept USDT for top-ups instead of only using cards?

A: Traditional card rails bring fixed fees, chargeback exposure, and cross-border processing friction. USDT top-ups can reduce those costs and make small, frequent reloads much more economical.

Q: Should merchants use TRC20 or ERC20 for virtual card reloads?

A: It depends on your audience and ticket size. TRC20 is often better for lower-fee, high-frequency reloads, while ERC20 can still matter for institutional or ecosystem-specific flows.

Q: How does CCPayment help prevent fake deposit webhook attacks?

A: CCPayment supports amount-less webhook notifications, HMAC verification, and server-side lookup through the Get Deposit Record API. That means your system credits balances only after confirming the authoritative deposit record.

Q: How can a platform protect margins when accepting USDT?

A: Use a low-fee gateway structure, choose the right chain for your users, manage gas allocation carefully, and convert funds into a stablecoin or settlement asset when needed. That keeps crypto top-ups aligned with your treasury strategy.

Crypto Adoption for Business 2026

Deep dives into Web3 payments, industry trends, and how to scale your global commerce with zero-code integrations.